The Best Detroit Car Accident Lawyers are at Michigan Auto Law

Our Detroit car accident lawyers have the experience, skills, resources and proven results to fight for you if you have been injured in a collision in the Motor City. With a law office located right in downtown, our car accident attorneys specialize in helping residents who have been injured in motor vehicle crashes or lost loved ones in wrongful death cases. For 50 years, our attorneys have been recovering record collision settlements and trial verdicts on behalf of our clients.

In fact, Michigan Auto Law attorneys have recovered more million dollar settlements and trial verdicts on behalf of our clients than any other attorney or law firm in Michigan. This means our Detroit car accident lawyers can help you to often resolve your case faster and for more money because our track record results in significantly higher settlements on behalf of our clients. All of this is within a culture of caring and communication and a reputation in the legal community for the highest ethics and integrity within the legal profession.

The Most Awarded Car Accident Attorneys In Detroit

Michigan Auto Law attorneys are also the most awarded in the city and in the state. Michigan Auto Law has consistently been named by independent third-party attorney review organizations and the news media as being among the “Best Lawyers” and “Best Law Firms” not just in Michigan, but in the entire U.S. We also have more attorneys ranked as “Super Lawyers” than any other Michigan personal injury law firm, including two attorneys ranked among Michigan’s top 50 lawyers in the state, in a review of over 60,000 Michigan attorneys of all areas of legal practice.

What’s more important than the legal honors and awards our attorneys receive from Hour Detroit and Crain’s Detroit Business are the reasons behind them: our Detroit car accident attorneys work harder to help our clients and their families get through what is likely one of the most difficult, emotional and stressful experiences in their lives, and we do it with caring and communication. The recognition and the honors and awards we receive reflect the hard work, caring and communication that our attorneys put into helping you.

Our mission at Michigan Auto Law is simple: to be the best Detroit car accident attorneys in Michigan every year. That means treating every client we help with dignity, respect, and caring. It means working incredibly hard and marshaling all of our experience, skill, dedication and grit to get our client the best possible legal results. Call our Detroit car accident lawyers for a free consultation. We are here to help.

Over 2,000 5-Star Reviews

Michigan Auto Law attorneys always provide personalized, compassionate attention to our clients. We have received over 2,000 five-star reviews because we work harder to keep our clients informed throughout the case process, answering every question promptly and doing everything we can to make challenging times easier for you.

★★★★★

Brandon Hunter from Detroit, MI

My case was unique but Michigan Auto Law was still willing to help. Staff was responsive, helpful and kind made me feel like they where genuinely cared. My attorney has a great response time also and was very communicative. I would recommend and use their service in the future.

Michigan Auto Law has been consistently named among the Top Lawyers in Detroit by Dbusiness Magazine, Hour Detroit, and Crain’s Detroit Business. Our Detroit car accident attorneys are also the go-to legal experts for print, radio and TV in Metro Detroit for stories about Michigan’s auto No-Fault insurance law and to provide legal analysis and commentary when a tragic motor vehicle crash has occurred. Michigan Auto Law attorneys are regular guests and have been interviewed on-air by Fox 2 Detroit’s Roop Raj, Huel Perkins and Charlie Langton and WXYZ’s Kim Russell and Jennifer Ann Wilson. Steven Gursen is also a frequent guest lecturer at Wayne State University Law School and the University of Detroit Mercy School of Law.

Our Detroit car accident lawyers consider the Motor City home. With our law offices in the Ford Building in the heart of downtown, just one block south of Campus Martius Park, Michigan Auto Law attorneys have long been active in giving back to the community. Every year, we hold a Forgotten Harvest volunteer event and we support the Wayne Metropolitan Community Action Agency’s annual Walk for Warmth. We are also members of the Downtown Detroit Partnership.

How Our Detroit Car Accident Lawyers Can Help You

Our Detroit car accident lawyers specialize in helping people who have been injured in motor vehicle crashes. We have been helping victims in the Motor City for more than 50 years and our results are better than any other personal injury attorney or law firm in Michigan. Michigan Auto Law attorneys have recovered more million dollar settlements and trial verdicts on behalf of our clients than any other attorney or law firm in Michigan.

We make sure you understand 100% of your legal rights after a crash and our Detroit car accident attorneys are here to help you with all aspects of your claim, including:

Ensuring that you are receiving all of the No-Fault insurance benefits you are entitled to

Investigating and verifying all of the insurance and coverage that may be involved in your case

Getting you the best possible settlement as quickly as possible.

Our Detroit car accident attorneys will help you navigate Michigan’s auto No-Fault insurance law and recover the financial compensation you deserve from a negligent and careless driver.

We also guarantee that our service will exceed your expectations. If you aren’t 100% satisfied, there’s no obligation and you pay $0 in fees. We also guarantee that our Detroit car accident attorneys will win and recover for you – or you won’t pay a dime.

Do I Need A Lawyer For A Car Accident In Detroit, MI?

If you are injured in a car accident in Detroit, MI you are not required to hire a lawyer but it is in your best interest because an experienced attorney can help protect your legal rights to collect Michigan No-Fault wage loss and PIP benefits and get your medical bills paid. Michigan’s No-Fault law can present many potential hurdles for the uninformed consumer.

Take, for example, providing “notice” if you are injured in a hit and run or injured by an uninsured driver. Many insurance policies have contract language requiring 30 days notice to recover uninsured motorist protection if you are injured in a hit and run collision, which unfortunately can be common with approximately 50% of all drivers in the Motor City driving uninsured. Failing to comply with the “notice” requirement in your own “uninsured motorist” policy will mean your policy will be voided and you lose the ability to recover compensation for your injuries and losses, leaving you with nothing – or worse yet, leaving you with lots of expensive medical bills to pay out of pocket and no insurance to pay for needed medical care and treatment in your future.

An experienced Detroit car accident attorney can protect you from traps for the unwary. Sadly this lately includes auto insurance companies and claims adjusters who try to trick city residents who are already under financial pressure into “settling” their injury claims for much less than they’re worth and forfeiting all of their future legal rights to No-Fault benefits and pain and suffering compensation.

Our Detroit car accident lawyers are here to help you and protect you. We can make sure you receive everything you are entitled to after a crash from your own insurance company and from the insurance company of the negligent driver who caused your injuries. That’s why it’s so important to call and have a free consultation with an experienced Detroit car accident attorney immediately after any motor vehicle crash in which you are injured.

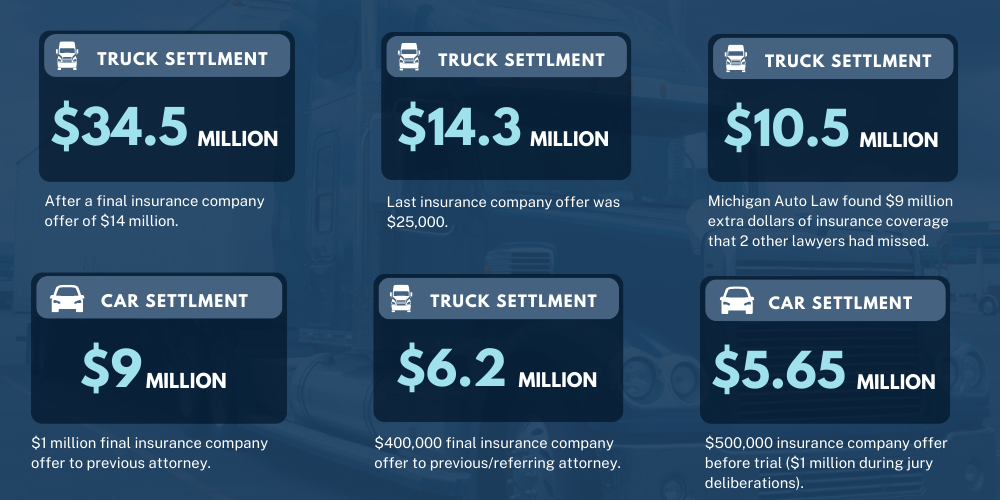

Our Results

More Detroit Car Accident Lawyer FAQs

What else do you need to know if you’re considering hiring a Detroit car accident lawyer? If you or a loved one are injured in a collision, you may be entitled to important benefits, pain and suffering compensation and other economic damages. But it’s important to remember that you’re more likely to recover the full value of your claim if you hire the right legal team to protect you and to protect your legal rights. Read our attorney FAQs below or call to speak to an experienced attorney for free with no obligation now.

Is it worth getting a lawyer for a car accident in Detroit, MI?

If you are injured in a car accident in Detroit, MI, it is worth getting a lawyer because the insurance industry has conducted their own research showing that people who are represented by experienced car accident attorneys recover more than people who are not represented by attorneys.

Also, at Michigan Auto Law, you don’t pay unless we win. Our Detroit car accident attorneys will handle all aspects of your injury case so you can focus on recovering and trying to put your life back together. We are always here to answer any questions about the case, the process, the law, the insurance company, the adjuster, the judge or anything else. We’re here for you.

How much does a Detroit car accident lawyer cost?

In Detroit, MI, a car accident lawyer doesn’t cost you anything unless they win your case. A one-third (1/3) contingency fee is the fee arrangement that most auto accident attorneys will charge in Michigan. An attorney cannot charge a contingency fee in excess of 1/3 or 33%.

At Michigan Auto Law, we will never ask you to pay any attorney fees unless and until we win your case. You do not pay anything up front or out-of-pocket. Our attorneys are paid at the end of the case and only if a recovery is made for you first.

On top of that, you and each and every one of our clients will get our 100% client satisfaction guarantee.

Do I need to get a lawyer for a car accident that isn’t my fault in Detroit?

You are not legally required to hire a Detroit car accident lawyer after a vehicle crash that isn’t your fault. But it’s in your best interest to do so. An experienced attorney, like the ones at Michigan Auto Law, who specialize in car, truck and motorcycle crash cases, will ensure you get the best possible legal settlement.

Your attorney can help insure that you receive all of the medical benefits and lost wages payments you’re entitled to – both now and in the future – under the auto No-Fault insurance law as well as pain and suffering compensation and other economic damages. The right attorney can help you win compensation and protect your legal rights, so you can focus on your medical recovery and getting back to fully living your life.

How long does a settlement take after a crash?

Each case is unique, so it’s a difficult question to answer how long does a car accident settlement take for a Detroit car accident lawyer. In general there are several factors that can help answer how long a settlement will take. These include: your injuries, prognosis and current future medical needs; whether you are partially or fully disabled from working; whether your injuries have resulted in an impairment that affects your ability to lead your normal life; whether your injuries will necessitate “excess” coverage for medical bills and lost wages; the experience, track record and reputation of your attorney (attorneys known for going to trial can settle cases for money and often much faster); the at-fault driver’s auto insurance company, adjuster, defense attorney and liability limits.

Injured in a car accident in Detroit? Call the attorneys at Michigan Auto Law

If you are injured in a car accident in Detroit, MI, call now (800) 968-1001 for a free consultation with one of our experienced Detroit car accident lawyers. There is no cost or obligation. You can also visit our contact page or use the chat feature on our website.

Michigan Auto Law is Michigan’s largest and most successful law firm that specializes exclusively in helping people who have been injured in auto accidents.

Our secret? Our car accident attorneys deliberately handle fewer cases than other personal injury law firms. This allows us to focus more time and attention on our cases.

Unlike other law firms, our attorneys are never too busy to promptly return phone calls and answer questions.

We have more than 2,000 5-Star Reviews that reflect this care and attention to detail.

More importantly, this client-focused approach leads to better and faster settlements for our clients. Michigan Auto Law has recovered more million-dollar settlements and trial verdicts for motor vehicle accidents than any other lawyer or law firm in Michigan. We’ve also recovered the highest ever reported truck accident and car accident settlement in the state.

Call our Detroit car accident lawyers now so they can start making a real difference for you.

Michigan Auto Law – Auto Accident Attorneys has full lists of the most dangerous intersections in Detroit, Wayne County and across the state: