U.S. DOT’s ‘Federal Automated Vehicles Policy’ urges $5 million in liability insurance coverage for road-testing self-driving cars, determining manufacturer liability for car accidents. Yet, neither issue addressed in MI Senate Bills 995-997

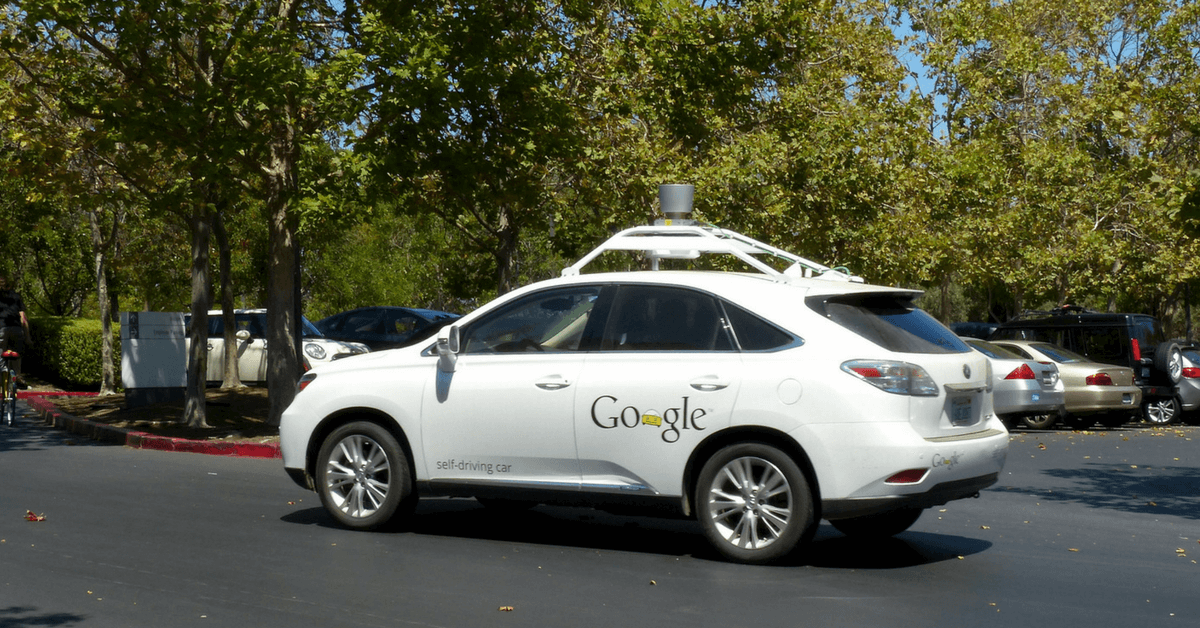

I’m 100% in support of the driverless car legislation that’s on its way to Gov. Rick Snyder for his consideration. It’s an important and vital step toward a future where self-driving cars will save thousands and thousands of lives every year:

- “Automated vehicles have the potential to save thousands of lives …” – U.S. Transportation Secretary Anthony Foxx

- “[T]he Department of Transportation has been exceptionally forward-leaning on automated vehicles” because “the promise of automated vehicles” is that “we could potentially prevent or mitigate 19 of every 20 crashes on the road.” – NHTSA Administrator Mark Rosekind

But Michigan’s driverless car legislation can still be improved

But my enthusiastic optimism doesn’t mean I don’t also think there’s room for improvement in the legislation, Senate Bills 995-997, which cleared both the Michigan House and Senate on November 10, 2016.

Specifically, the bills inexplicably – and unwisely – fail to follow the recommendations in the “Federal Automated Vehicles Policy,” released by the U.S. Department of Transportation in September 2016, in two crucial areas:

- Establishing the minimum amount of insurance coverage required for road-testing autonomous cars.

- Determining when manufacturers of driverless cars will be liable for car accidents caused by an autonomous vehicle they produced.

The state of Michigan wants to be a leader in autonomous vehicle development, but this isn’t the way to get there. We should not be hastily pushing out new laws that only deal with some of the issues that the politicians want to address – while avoiding the thorny and complicated, but essential, ones – such as what happens after a car accident involving a driverless car and what will be the minimum insurance coverage available to protect accident victims and a nascent autonomous manufacturing industry.

If Michigan wants to really be on the cutting-edge – and continue to be the “worldwide leader in automotive research and development” as the bills’ sponsor Sen. Mike Kowall (R-White Lake) has said – then one of the ways in which we can distinguish ourselves from other states is by being among the first in tackling in a comprehensive and thoughtful manner the issues of insurance and liability for driverless cars and their manufacturers.

Today, I want to share my thoughts on the insurance coverage issue for driverless vehicles. Tomorrow I’ll address liability when one of these autonomous vehicles causes a car accident that kills or seriously injures someone. Both issues must be addressed, not ignored, if Michigan is to be at the center of this transformative industry.

$5 million in road-testing insurance coverage

The U.S. Department of Transportation’s “Federal Automated Vehicles Policy” Guidelines states that, as part of the application process to “test HAVs [“highly automated vehicles”] on public roadways,” the HAV “manufacturer” “should” provide:

“[E]vidence of the manufacturer’s or other entity’s ability to satisfy a judgment or judgments for damages for personal injury, death, or property damage caused by a vehicle in testing in the form of an instrument of insurance, a surety bond, or proof of self-insurance, for no less than 5 million U.S. dollars.” (Federal Automated Vehicles Policy, “Application for Manufacturers or Other Entities to Test HAVs on Public Roadways,” page 42)

Additionally, in a footnote to the above statement, the Federal Policy observes that “[d]epending on the circumstances, States may wish to establish a higher minimum insurance requirement.” (Federal Automated Vehicles Policy, “Application for Manufacturers or Other Entities to Test HAVs on Public Roadways,” page 42, footnote 54)

That stands in stark contrast to what Michigan’s “automated vehicles” law currently provides – and would provide under SB 995-997.

Under the existing rules for road-testing self driving vehicles – which would be left unchanged by the concurred bills awaiting Gov. Rick Snyder’s review – all that a manufacturer must have in the way of insurance coverage is the minimum liability limits that all Michigan cars must have: $20,000 in personal injury liability and $10,000 in property damage liability. (MCL 257.665(1); 500.3101; 500.3009(1))

That’s insane.

So it’s $5 million versus $20,000. Whether you’re a manufacturer of this technology or an accident victim, which makes you feel more secure and protected?

Which makes you more confident you’ll receive the pain and suffering compensation you deserve if you’re completely innocent and injured in a car accident caused by a driverless car?

I realize some people may say, “What do you expect? Steve Gursten is an auto accident attorney; of course he wants $5 million in insurance coverage instead of $20,000.”

The fact that it will better help the people who I represent, however, doesn’t mean it isn’t also the best way to protect the manufacturers and developers of autonomous vehicle technology. In addition, it can position Michigan as a state where manufacturers can confidently invest and develop this transformative technology, without worrying about the possibility of being put out of business by lawsuits when these cars do cause crashes – as they most certainly will.

The key is for us to remember that while driverless cars will cause car accidents, they will certainly cause far less than we cause today as all-too-human drivers who text and drive and do all sorts of unsafe things when behind the wheel.

There will be winners and losers in the race by various states to be a leader in the manufacturing of this technology, and I want Michigan to be a winner.

If, in the process of this becoming reality, one day it makes my job as an auto accident attorney obsolete, then all the better. Until then, let’s not ignore the insurance issue as Senate Bills 995-997 would do.